LABUAN NON-PURE INVESTMENT HOLDING COMPANY

A Non-Pure Investment Holding Company in Labuan differs from a Pure Investment Holding Company in that it allows broader income streams beyond just dividends and capital gains from equity holdings. Specifically, it can earn income from sources such as interest, rental income, royalties, and other types of passive income related to asset management. This makes a non-pure holding company suitable for investors or businesses managing diversified assets, including real estate, bonds, mutual funds, or other financial instruments, providing more flexibility in income generation.

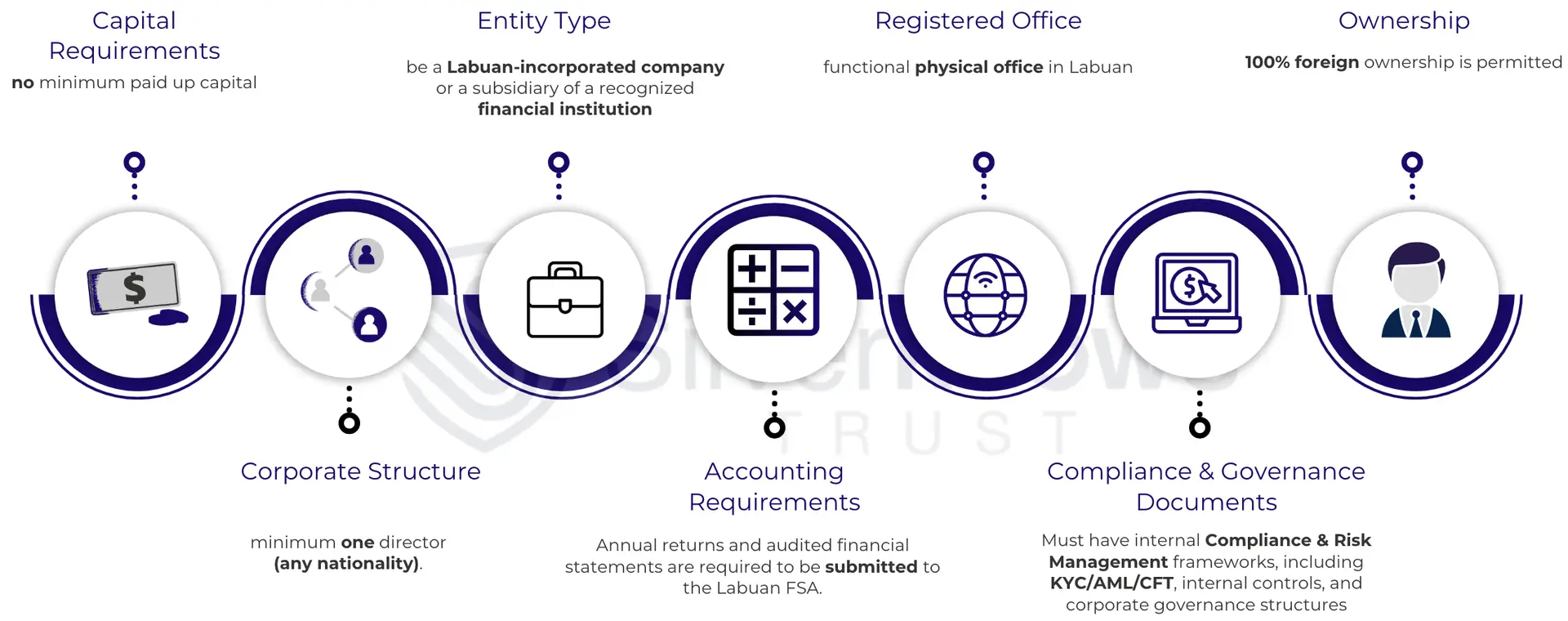

Operation Requirements

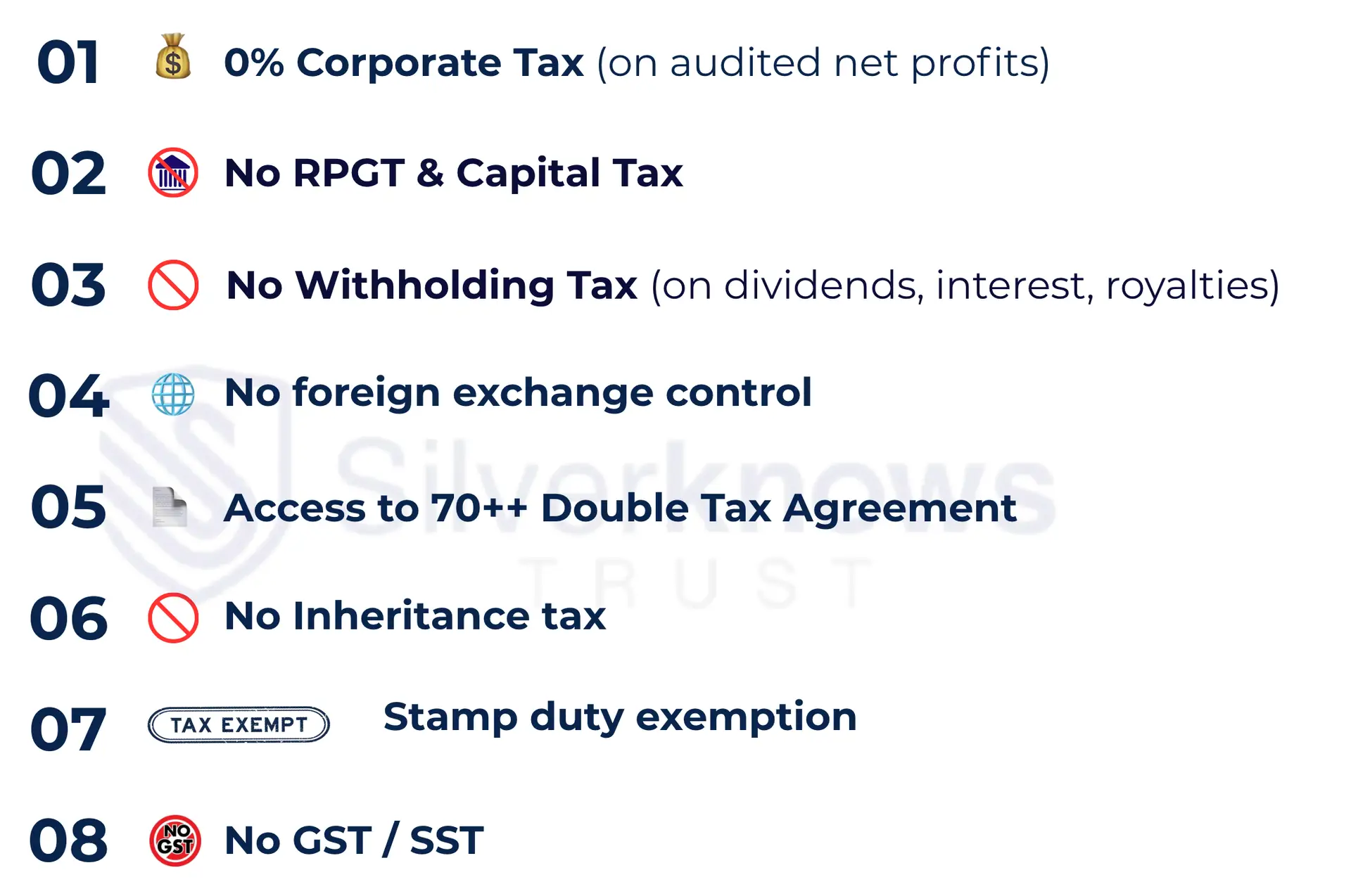

Tax Benefits

Labuan Tax Substance Requirements under LBATA 1990

| Labuan Trading Entity | 🧑💼 Minimum number of Full Time Employee (Living in Labuan Resident) | 🏢 Functional Physical Office (in Labuan) | 💰 Operating Expenses / Year (in Labuan) |

|---|---|---|---|

|

Non-Pure Investment Holding Company |

1 |

Yes |

RM20,000 |

Documents Required to Establish a Non-Pure Investment Holding Company

Formation Procedure & Estimated Processing Timeline

Our Services

We offer comprehensive assistance for the formation of your Labuan Non-Pure Investment Holding Company:

Our scope of services Include:

- Incorporation of a Labuan company

- Strategic advisory on company structure and shareholding design

- Tax planning and advisory services

- Advisory on compliance with the Labuan Financial Services and Securities Act 2010 (LFSSA 2010)

- Provision of a detailed documentation checklist

- Conduct of due diligence checks on applicant(s)

- Preparation and reservation of company name

- Preparation and submission of application to Labuan FSA

- Provision of first-year Resident Secretary and Registered Office services

- Preparation and filing of tax returns, annual returns, and AGM documents with Labuan FSA

- Structuring of organizational chart and governance framework

- Guidance on meeting substance requirements under Labuan regulations

- Opening of one (1) multi-currency bank account in Kuala Lumpur or Labuan

- Provision of custodian or stakeholder services

- Provision of nominee director or shareholder services

🚀 Begin Your Journey with Confidence

With comprehensive, end-to-end services spanning incorporation, tax planning, regulatory compliance, and banking facilitation, Silverknows Trust Ltd is your trusted partner in establishing efficient and resilient business structures.

Let us help you unlock the full potential of Labuan's global advantages.

Contact:

General Line: +603-9543 1882 Business Enquiry: +6012-2600 633

Email:

hello@silverknows.com

Office Hours:

Mon-Fri: 8.30am - 5.30pm